Business owners frequently equate profitability with financial health. However, profit and cash flow measure distinct financial dimensions. Understanding the difference is essential for maintaining liquidity and long-term viability.

1. Profit Defined

Profit represents revenue minus expenses within an accounting period. It appears on the income statement and reflects operational efficiency. However, profit includes non-cash items such as depreciation and accrued revenue.

2. Cash Flow Defined

Cash flow measures actual inflows and outflows of cash. It determines whether a business can meet short-term obligations. Positive profit does not guarantee positive cash flow.

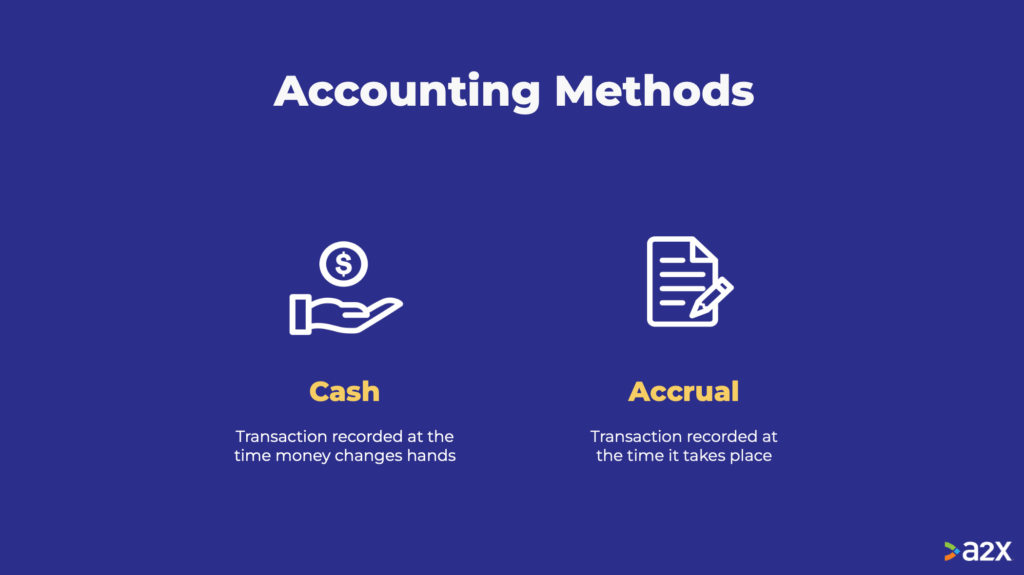

3. Timing and Accounting Methods

Accrual accounting records revenue when earned, not when received. Expenses may be recorded before payment. These timing differences explain why profitable businesses may face liquidity constraints.

4. Strategic Financial Management

Balancing receivables, payables, and inventory levels improves cash flow stability. Monitoring operating cash flow ensures sustainable operations even during growth phases.

Conclusion

Profitability indicates efficiency, but liquidity ensures survival. Businesses must analyze both metrics to maintain operational continuity and financial resilience.